Smaller footprint. Shared amenities. Big homeownership opportunities.

Thinking about buying a condo? Whether you’re a first-time buyer, a downsizer, or looking for a low-maintenance lifestyle, financing a condominium comes with unique opportunities — and a few added considerations.

At Choice Mortgage Group, we help simplify the condo financing process with personalized guidance and transparent communication. Our goal is to help you secure the right mortgage for your condo purchase, whether you’re buying in a high-rise downtown or a detached condo in a suburban community.

Thinking about buying a condo? Whether you’re a first-time buyer, a downsizer, or looking for a low-maintenance lifestyle, financing a condominium comes with unique opportunities — and a few added considerations.

At Choice Mortgage Group, we help simplify the condo financing process with personalized guidance and transparent communication. Our dedicated Condo Desk will review the condo project before you make an offer or list your property for sale to help ensure a smooth transaction and present all your conventional and portfolio options. Our goal is to help you secure the right mortgage for your condo purchase, whether you’re buying in a high-rise downtown or a detached condo in a suburban community.

What is a Condo?

A condominium, or condo, is a type of property where you own your individual unit — typically everything inside the walls — while sharing ownership of common areas such as the lobby, pool, gym, elevator, parking garage, and outdoor spaces.

Unlike single-family homes, condos operate under a Homeowners Association (HOA), which manages the maintenance, amenities, and community rules. Condo owners pay monthly dues to the HOA, which go toward upkeep and services.

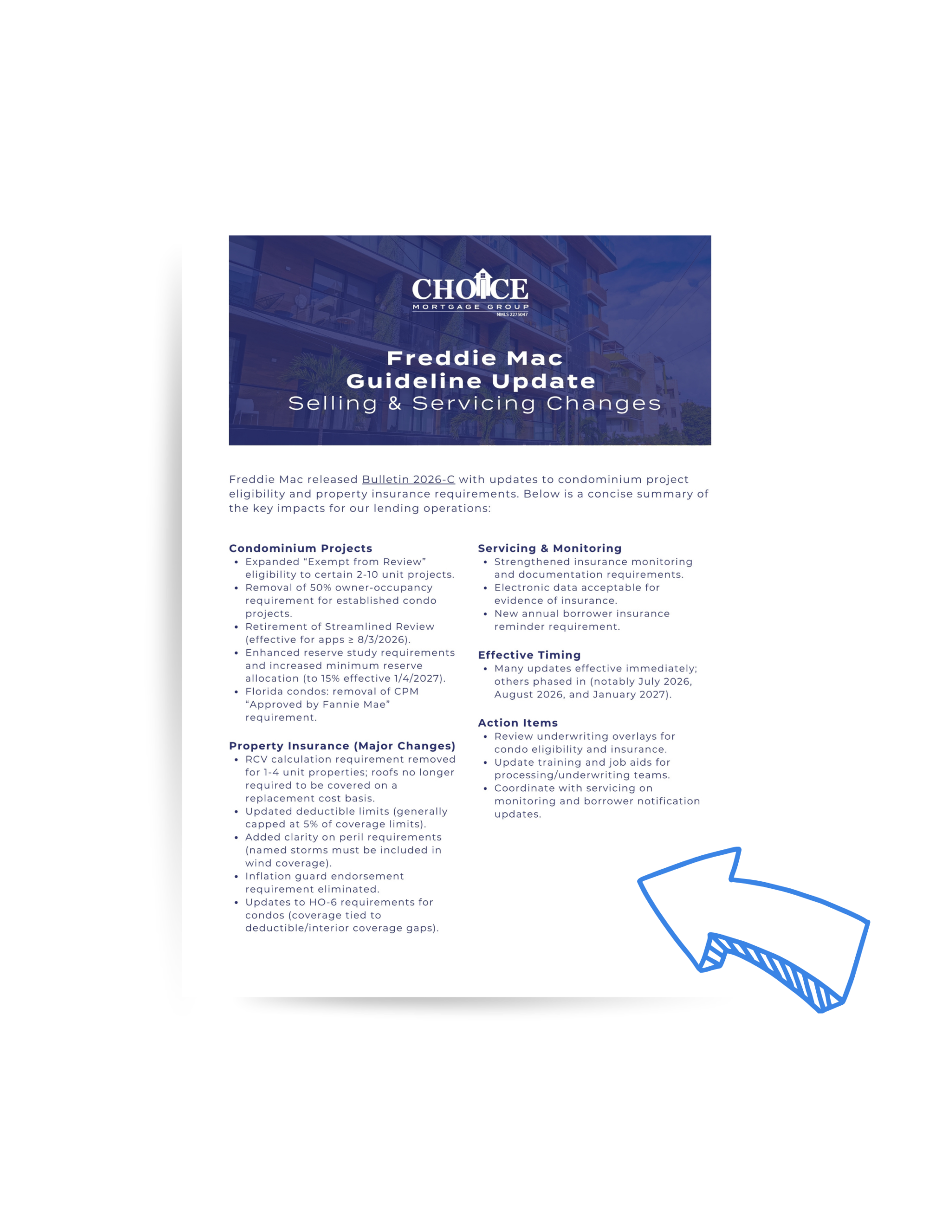

Big Changes Coming to Condo Financing

New lending updates are creating opportunities for buyers today—while also introducing important changes that could impact financing options in the near future.

Condo living can be a great fit for buyers who value convenience, location, and community — but it’s important to understand that condo loans require a bit more review, especially around the property itself.

Key Benefits of Condo Ownership

Lower maintenance

(HOA takes care of most exterior and shared spaces)

Desirable locations

often closer to city centers or coastal areas

Access to amenities

like pools, gyms, and outdoor space

Lower purchase prices

compared to single-family homes in many markets

Strong investment potential

in high-demand areas

What to Know About Condo Financing

Condo loans require two levels of approval — for you as a borrower, and for the condo project itself. This is because lenders want to ensure the entire property is financially sound and properly managed.

At Choice Mortgage Group, we specialize in navigating condo loan approvals, even when other lenders can’t. We’re familiar with spot approvals, warrantable vs. non-warrantable condos, and how to get your deal across the finish line — even if your condo project has been denied by another lender.

Common Factors That Can Impact Condo Approval

Percentage of owner-occupants vs. renters

Delinquent HOA dues

Pending litigation

Reserve funds and insurance coverage

Commercial space ratio

Veteran-friendly financing — with a few extra steps.

Buying a condo with a VA loan is absolutely possible — and often a great choice for eligible veterans and active-duty service members seeking low-maintenance homeownership. But there’s one important distinction: the condo complex itself must be VA-approved before you can use your VA loan there.

This extra layer of review exists to ensure that veterans aren’t burdened by restrictive HOA rules, poor financial management, or unfair community requirements. It’s all about protecting your interests — and the integrity of the VA loan program.

What does VA condo approval involve?

Before your loan can move forward, the Homeowners Association (HOA) or condo developer must have submitted the community to the Department of Veterans Affairs for review and received formal approval. This approval covers financial stability, insurance coverage, occupancy levels, HOA fees, and other criteria designed to protect VA borrowers.

If you're eyeing a condo property, we’ll help you

Check the VA approval status of the condo complex

Explore alternative options if the condo is not yet approved

Work with the HOA to initiate the approval process, if needed

Compare other loan options if VA financing isn’t a fit

Townhomes and row homes may also fall under the same VA rules, depending on how the property is structured and titled.

Let’s Get You Started

Take the first step today. Complete our pre-approval form and see how much home you can afford